Dollar rally sparks sharp gold sell off

Precious metals fell sharply in June 2021, with gold, which fell by more than 7%, recording one of its largest monthly declines of the last decade.

The key driver of the sell-off was as a more hawkish US Federal Reserve, which brought forward its projections for when monetary policy in the United States may tighten, sparking a rally in the value of the US dollar. The pullback in precious metals, while frustrating for bulls, has seen sentiment and technical indicators hit levels that are often seen when the market is close to bottoming.

Summary of market moves:

- Gold and silver prices suffered major falls in June, with the two precious metals down by 7% in US dollar terms.

- Prices for the two precious metals in Australian dollar terms fell by closer to 4.5%, owing to a 2.5% decline in the AUDUSD FX rate, which ended June at 0.752.

- A more hawkish tone by the US Federal Reserve, which sparked a rally in the US dollar was the primary driver of the pullback in precious metal prices, with real yields largely unchanged for the month.

- Sentiment toward precious metals was negatively impacted, while technical readings also suggest the market is oversold.

Full report - June 2021

Gold and silver prices experienced sharp falls during June, with the 7% decline in the gold price representing the sixth largest monthly fall since the start of 2010, with the 10 largest monthly corrections over this time period highlighted in the table below.

Month

Decline in gold price (%) during month

End of month gold price (US dollar per troy ounce)

June 2013

- 11.1

1,233

September 2011

-11.0

1,623

December 2011

- 10.4

1,564

November 2016

-8.2

1,173

April 2013

-7.5

1,477

June 2021

-7.2

1,763

November 2015

-6.8

1,064

July 2015

-6.6

1,095

February 2021

-6.5

1,743

November 2020

-6.3

1,763

Source: The Perth Mint, World Gold Council, LBMA

Interestingly, two of the other top 10 monthly price declines (February 2021 and November 2020) were also part of the current corrective cycle that dates back to the middle of August last year, when gold was trading at all-time highs above USD 2,050 per troy ounce.

This helps highlight how difficult the last nine months have been for precious metal bulls, and how it has come to pass that gold has actually fallen over the 12 months to end June. While that might seem hard to fathom given the events of the last year, which would have been expected to drive the price of safe haven assets higher, it’s worth highlighting the fact that gold is still up 16% since the start of 2020, when the world first started appreciating the COVID-19 threat.

Gold also remains almost 50% higher compared to September 2018, which was around the time developed market central banks began easing monetary policy in an effort to stimulate flagging levels of economic growth.

While the longer term return figures for gold remain impressive, there can be no doubt that the recent weakness has shaken the faith of certain segments of the precious metals market. June saw a notable decline in bullish positioning in the futures market, particularly in the latter part of the month, while ETFs also saw outflows, which we explore below in more detail.

The recent weakness also saw sentiment toward precious metals take a significant hit, while technical indicators have now fallen to levels that often coincide with market bottoms.

What has driven the pullback in gold?

The recent sell off in precious metals was mostly attributed to a more hawkish than expected Federal Reserve, whose June policy meeting now has the market expecting an earlier return to interest rate hikes, which could now occur in 2023.

This is not to say the Fed is in a rush to walk back the extraordinary stimulus it is providing markets, and indeed in its June policy meeting it reaffirmed the commitment to purchase USD 120 billion per month of Treasury and mortgage backed securities and maintain the Federal Funds rate between 0 - 0.25%, among a range of other policy tools currently being deployed.

Nevertheless, the market’s interpretation of a change in tone from the Fed helped push the US dollar higher (the US Dollar index is now up over 3% since the late May lows), and in the short-term also caused real yields to jump, with both of these factors helping drive the sell-off in gold.

Short-term price moves aside, we think there are at least five factors that have driven the gold price correction since August of last year, with the precious metal now down 15% from the all-time highs seen back then.

Those factors include a stabilisation in real yields, strong stock market performance, rising economic optimism as the threat of COVID-19 recedes (as hard as that may be to believe in Australia right now), the attention that Bitcoin and cryptocurrencies have generated, and last but by no means least, the level of froth that existed in precious metal markets nine months ago.

Stabilisation in real yields

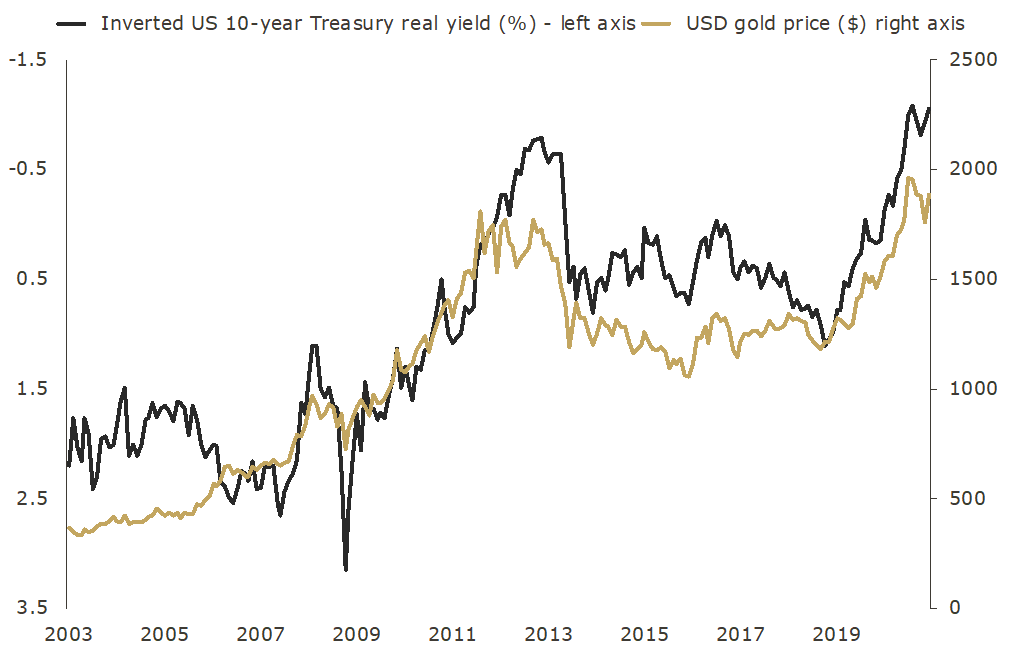

Over the long run, gold prices are highly correlated to real yields, which is logical given the real yield available on credit (but not inflation) risk free US Treasury bonds are one of, if not best, indicators of the opportunity cost of owning an income free asset like gold.

The chart below, which highlights the US dollar gold price and the real yield on a 10-year US Treasury bond from 2003 to the end of 2020 illustrates the relationship between the two.

US dollar price of gold and real yield on a 10-year US Treasury

Source: The Perth Mint, Reuters, US Treasury, St Louis Federal Reserve

Since gold peaked in August 2020, real yields for longer dated US Treasuries, which are those with 10, 20 or 30-year maturities, have increased -, which is to say they are now less negative than they were nine months ago. This can be seen in the table below.

Date

5 year

7 year

10 year

20 year

30 year

Gold price

06/08/2020

-1.32%

-1.22%

-1.08%

-0.72%

-0.45%

2,067oz

30/06/2021

-1.60%

-1.21%

-0.87%

-0.41%

-0.21%

1,763oz

Source: United States Treasury

Strong stock market performance

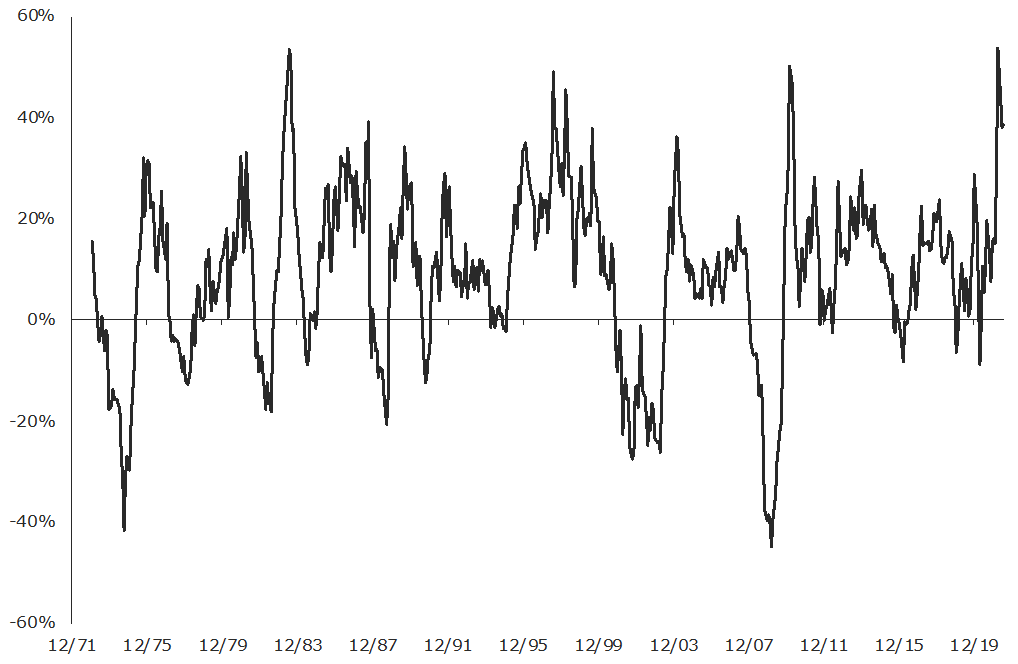

Since the COVID-19 induced market lows seen in March 2020, stock markets around the world have staged an almost unprecedented rally. In Australia for example, the ASX 200 is up more than 50%, whilst in America, the S&P 500 has almost doubled.

On a rolling one-year basis, the S&P 500 was up almost 40% in the year to end June, making the last 12 months one of the greatest market rallies of the last 50 years. This can be seen in the below chart, which highlights year on year movements in the S&P 500.

Rolling annual returns for the S&P 500

Source: The Perth Mint, Yahoo Finance

The rise in equity prices has also seen a meaningful shift in portfolio allocations, with investors upping their exposure to share markets. Indeed, data released from Bank of America Merrill Lynch in late June suggests equity allocations within client portfolios are now at all-time highs.

Furthermore, on an annualized basis, inflows into equities in the first six months of 2021 have been so significant that if they continue at their current pace for the rest of the year they will be substantially larger (circa 50%) than cumulative inflows for the past 20 years combined.

As a final sign of the exuberance in risk assets today, CFTC data suggests small speculators have never had more money invested in long, equity market futures contracts, which require the market to keep rising in order for them to make money.

While gold is typically positively correlated to rising stock markets, there is no doubt it really comes into its own during periods of market distress (for example in Q1 last year when it outperformed the stock market by almost 25%).

Given we are in the midst of such a strong stock market rally, and seeing so much money pour into equities, it’s no surprise the appetite for a safe haven asset like gold has waned over the past few months, putting downward pressure on prices.

Rising economic optimism

Despite the ongoing threat posed by COVID-19, optimism regarding the economic outlook has improved markedly in the past few months, driven by vaccine rollouts across most of the developed world, and fiscal stimulus measures which have supported cashflows for households and businesses.

Growth forecasts continue to be revised up, while consumer confidence in the United States is now soaring, with the latest Conference Board numbers suggesting confidence levels are back to where they were roughly 18 months ago before the pandemic hit.

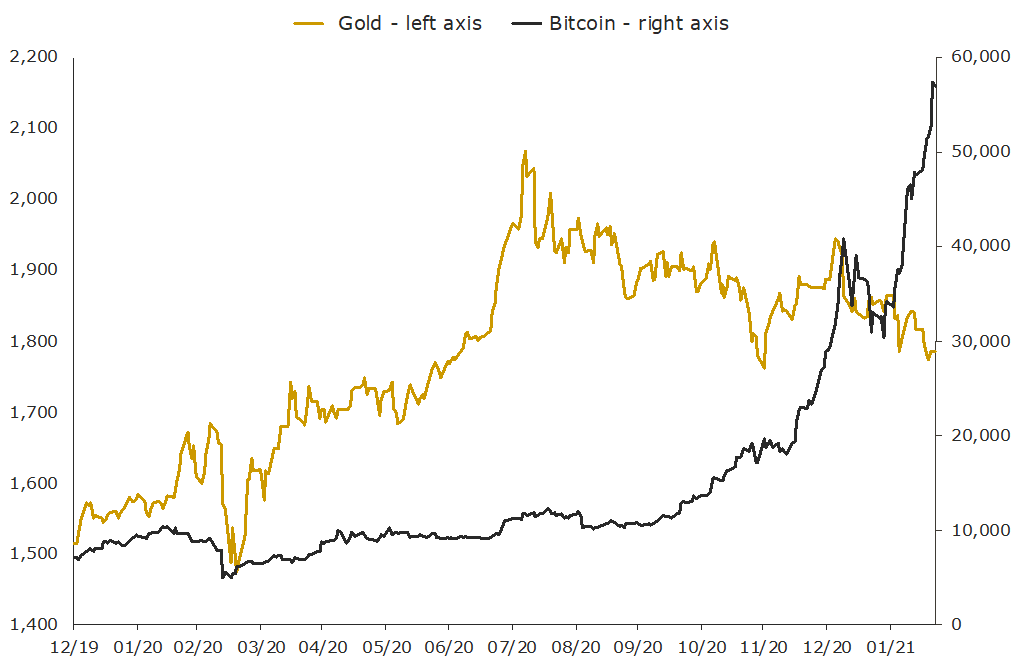

Bitcoin

Despite the 50% correction that we have seen in Bitcoin (BTC) prices in the past few months, it has been a very strong year for cryptocurrencies.

On the day gold peaked back in early August 2020, BTC was trading below USD 12,000 per coin. It then went on to rise almost five times over, trading at almost USD 65,000 per coin in mid-April this year.

Even after the correction it has had since that April high, the BTC price is still more than triple where it was when gold peaked, with the chart below (which comes from our late February research report: Gold, Bitcoin and the Elon effect, highlighting the price movements of the two assets since the start of last year.

While gold and BTC have very different risk profiles, the rise in the price of BTC and the attention that it has generated given the launch of BTC ETFs, the news that Tesla added BTC to its balance sheet, and the perpetual marketing of BTC as “digital gold”, have had some negative impact on gold in the past six to nine months.

Froth

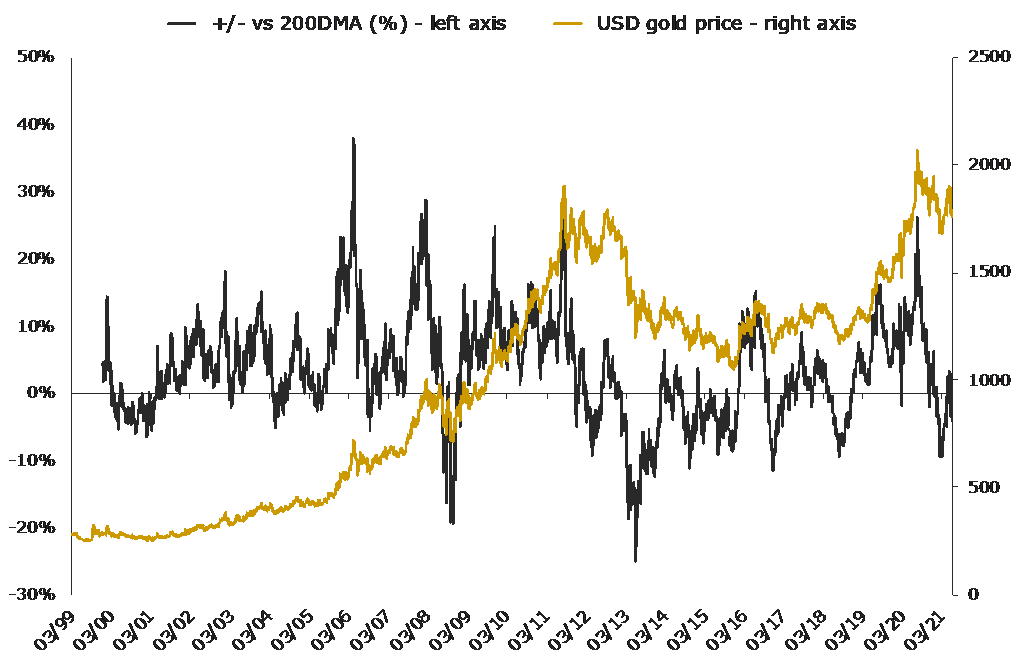

The final reason gold has corrected since August 2020 is simple. It was overbought and way too popular, with the move above USD 2,000 per troy ounce sparking a wave of bullish headlines and price forecasts, which often occur just before an asset is set to undergo a correction.

As we pointed out last year, gold was also trading at more than 20% above its 200-day moving average (200DMA), a level that often coincided with interim market tops, as the following chart highlights.

USD gold price per troy ounce and 200DMA

Source: The Perth Mint, World Gold Council

The good news is that as at the end of June 2021, gold was trading 4% below its 200DMA. That doesn’t mean the market has bottomed, but all the froth that was evident in the market in August is well and truly gone.

That’s a positive sign.

Physical markets, ETF flows and managed money positioning

Given the multiple factors that have driven the gold price correction over the last few months, it should come as no surprise that the demand picture for the precious metal has been a mixed bag in 2021. On the physical side of the market, volumes out of India, which had been robust initially, continue to be impacted by COVID-19.

Despite this, Swiss exports to Asia were climbing up until the end of April, helped along by the price pullback in Q1, though they then dropped by more than 50% in May as the USD gold price rallied back toward USD 1,900 per troy ounce.

The sharp gold price sell-off in late June reignited demand from China in particular, something The Perth Mint has seen first-hand with buyers returning to the market and adding to their holdings.

Perth Mint minted product sales also tell an interesting story, with Q1 seeing some of the highest levels of demand for gold and silver on record. Interestingly, in Q2, gold sales fell, with June being the slowest month since January, while silver continued to see impressive demand, which the following table attests too.

Time period

Average monthly sales - gold (troy ounces)

Average monthly sales - silver (troy ounces)

Q1 2021

110,312

1,531,041

Q2 2021

88,478

1,774,015

Source: The Perth Mint

In the gold ETF space, we’ve seen the better part of 145 tonnes of gold (4% of total global holdings) divested from these products in the first half of the year, though June only saw modest outflows.

Most of the outflows for the year have come from North American investors, with smaller outflows seen in Europe. Interestingly, investors in Asia are still continuing to accumulate gold through ETFs, including in Australia, where Perth Mint Gold (ASX:PMGOLD) saw inflows of almost 3,000 ounces (just over 1% of fund holdings) in June.

The futures market also tells an interesting story, which can be seen in the chart below. It shows net positioning amongst managed money speculators as well as the US dollar gold price since late 2009.

USD gold price per troy ounce and net managed money futures positioning

The chart highlights that increases in net positioning typically occur, and indeed contribute to rising gold prices, while the reverse is also true. Over the course of the first six months of this year, the net position almost halved.

This was predominantly driven by a more than 30% decline in long exposure, much of which occurred in the last two weeks of June, after the US Federal Reserve meeting.

While this has undoubtedly contributed to the recent price weakness in gold, long positioning has now fallen to levels seen near the bottom of corrective cycles.

That’s no guarantee that the next move in prices will be to the upside, though it should provide some encouragement to long-term investors happy to add to positions during pullbacks like the one we are experiencing now.

DISCLAIMER

Past performance does not guarantee future results. The information in this article and the links provided are for general information only and should not be taken as constituting professional advice from The Perth Mint. The Perth Mint is not a financial adviser. You should consider seeking independent financial advice to check how the information in this article relates to your unique circumstances. All data, including prices, quotes, valuations and statistics included have been obtained from sources The Perth Mint deems to be reliable, but we do not guarantee their accuracy or completeness. The Perth Mint is not liable for any loss caused, whether due to negligence or otherwise, arising from the use of, or reliance on, the information provided directly or indirectly, by use of this article.