Gold hit hard as bond yields and bitcoin soar

The gold price suffered its largest monthly fall in several years during February, as bond yields rocketed higher, and cryptocurrency prices soared. Gold ETFs saw substantial outflows, while sentiment toward precious metals has also soured, which is often a good sign for investors looking to add to their holdings.

Summary of market moves

- The USD gold price fell by 6.5% in February, one of its largest falls in years, with the precious metal finishing the month at 1742.85 per troy ounce

- AUD gold fell even further (-8.4%) ending the month below 2,250 per troy ounce, as the AUD continued to climb, ending February at USD 0.7829

- Silver fell by just 2.7% in February, supported by strength in broader commodity markets, which were up 6.5% for the month. The gold to silver ratio ended February at 65, having started the month closer to 68

- Bitcoin prices soared by 36% in February, though at one point they were up by almost 75% as news Tesla, led by CEO Elon Musk, invested USD 1.5 billion into the cryptocurrency fuelled price gains

- Bond yields soared globally, with the US 10-year yields rising by as much as 40% intra-month, ending February at 1.44%. Australian 10-year yields rose by more than 50%, ending the month at 1.69%

- Equity markets were positive during February, despite selling off in the last few trading days, with the S&P 500 rising more than 2.5% for the month.

Full report - February 2021

Precious metal markets fell sharply in February, with gold declining by more than 6% in USD terms. Silver held up better than gold, falling just 2.7%, with the metal supported by broader strength in commodity prices and a more bullish outlook for global economic growth.

While the pullback in gold may have alarmed some investors, it was unsurprising, given the market movements and economic developments that took place during February.

The most important of these was movements in the bond market. During February, bond yields rose, with the US 10-year treasury yield increasing by almost 40% in the space of a few weeks, as markets priced in both a faster economic recovery, and a speedier return to monetary tightening.

Indeed, this spike in bond yields saw bond market prices (which move in the inverse direction to yields), suffer one of their largest declines in years.

Inflation expectations also eased, with US 5-year, 5-year forward inflation rate expectations falling by almost 10% in the last two weeks of February, to end the month at just 1.91%.

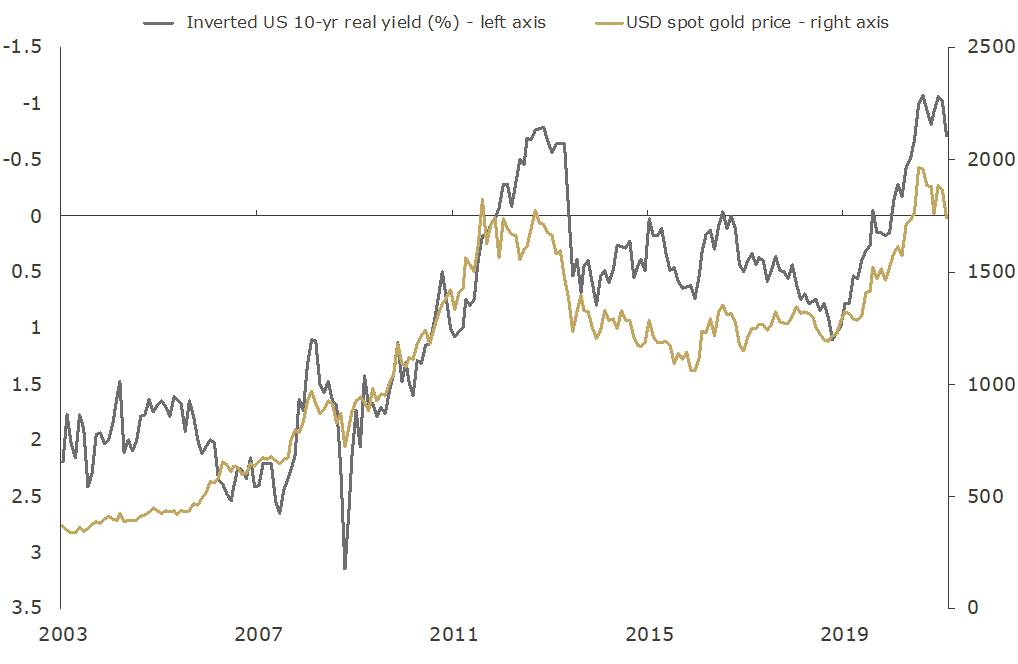

Higher nominal yields and lower inflation expectations combined to see real yields on treasury securities rise, with the real yield on US 10-year treasury securities seeing a 30% increase across the course of the month, from -1.01% to -0.70%.

Crucially, despite these moves, real yields remain negative out to 20 years, which is the key point for long-term asset allocators.

Short-term, it should be no surprise the increase in real yields presented a headwind to gold, with the correlation between the two clear in the chart below, which dates back to 2003.

USD gold price and real yield on 10-year US treasury bonds

Source: The Perth Mint, World Gold Council, US Treasury

On top of developments in the bond market and on the inflation front, we also saw a continued rise in equity markets, and very strong investor inflows for risk assets. As an example, a report in late February suggested more than USD 45 billion had been invested in equity markets in the previous week, the third-largest inflow on record.

We also saw surging interest in cryptocurrencies (more on this below), which at the margin will have negatively impacted gold demand.

Finally, February saw unambiguously good news in terms of getting on top of the COVID-19 challenge in the United States, with record falls in the number of confirmed cases, hospitalizations and people passing away from the disease.

Add all these factors together and it’s no surprise that the investor appetite for a safe haven asset like gold declined during February, which largely explains the pullback we saw.

Where do things stand now?

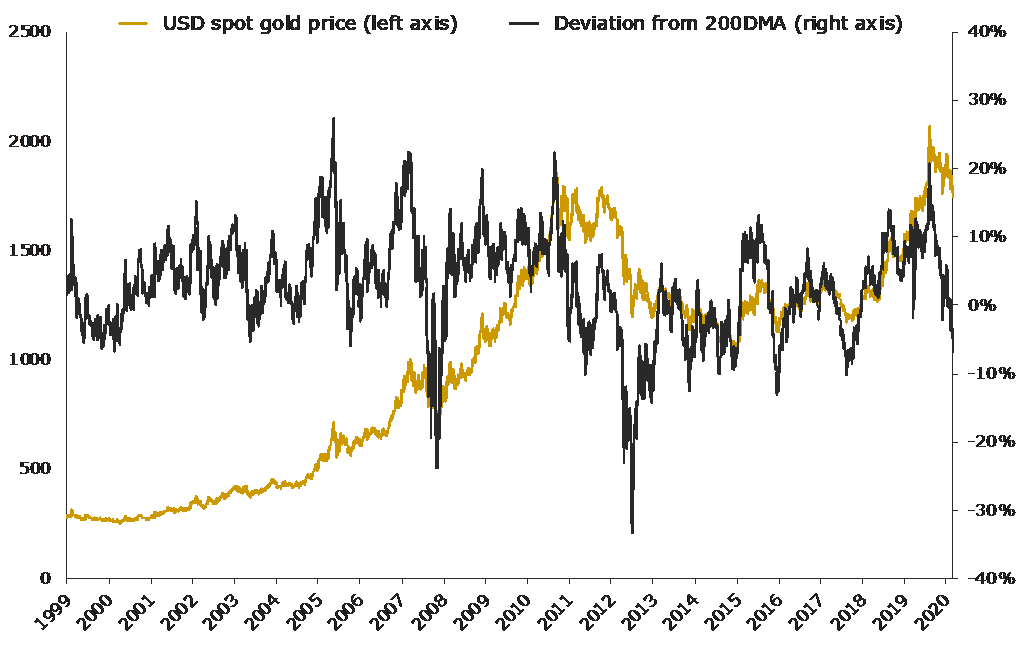

Given gold has corrected by almost 16% in USD and 22% in AUD terms since the August 2020 high, it should be no surprise that market participants are far more sceptical about the outlook for bullion, and more cautiously positioned.

This can be seen through a number of data points, including;

Futures market positioning

Managed money long positions dropped to just 140,000 contracts by the 23 February, down more than 30% since the start of the year. Managed money short positions on the other hand have increased by 22% in the last month.

ETF flows

Preliminary data suggests that around the globe, gold ETFs have seen close to 40 tonnes of outflows in February. In the last week alone, the world’s largest gold ETF saw almost USD 2 billion come out of the product, which is the largest single week for outflows since gold prices corrected sharply back in 2013.

Sentiment

Back then, the price was trading at more than 20% above its 200-day moving average (200DMA), which was a clear warning sign that the rally was getting ahead of itself. The situation is completely different now, with gold ending February roughly 6% below its 200DMA.

USD gold price and deviation from 200DMA

Source: The Perth Mint, World Gold Council

Gold vs bitcoin

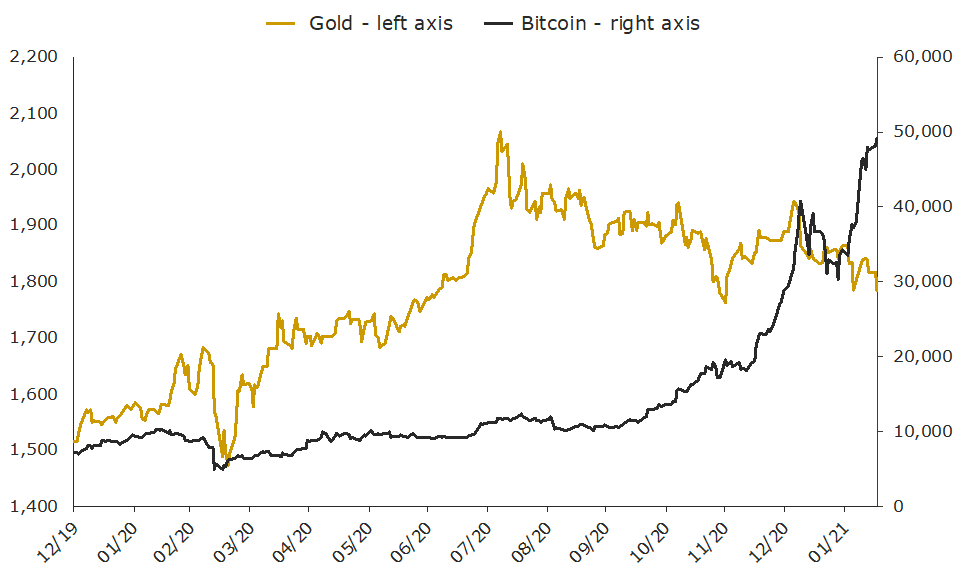

The rise in the bitcoin price, and the news that Tesla added the cryptocurrency to its balance sheet, which was announced in early February, have made digital gold front page news again.

Everyone is talking about it once more, from Berkshire Hathaway’s Charlie Munger, who said “I never buy any bitcoin”, to the world’s largest hedge fund, Bridgewater, which said bitcoin may continue to grow if volatility and liquidity issues are resolved, while the uncertain regulatory environment for cryptocurrencies remain another risk factor.

Given the rally in bitcoin has coincided with the pullback in gold that we have seen since early August 2020, there are now no shortage of commentators stating that the precious metal is being usurped by its digital counterpart, with some going so far as to encourage investors to drop gold, and reallocate to bitcoin instead.

Gold and bitcoin prices – December 2019 to February 2021

Source: World Gold Council, LBMA, Coinmetrics, Coindesk, data to Sunday 21 February

Our latest report; Gold vs Bitcoin? What you need to know about these two very different asset classes, questions this narrative, looking at the various metrics by which investors can, and indeed should, compare these two very different asset classes. As the report highlights, gold still has many advantages over bitcoin.

Outlook

A continued rise in bond yields could also be an ongoing headwind, though a case can be made precious metals may actually see some safe haven demand in this environment if higher yields cause some kind of deflationary shock and/or a more meaningful stock market correction, with equities pulling back in the last couple of days in February.

It is also worth noting too that central banks will be closely watching said bond yields and may well increase both qualitative and quantitative interventions in the market if recent developments have too much of a negative impact on financial markets.

Indeed, we are arguably already seeing this in Australia with the RBA doubling its purchases of government bonds from AUD 2 billion to AUD 4 billion on Monday 1 March, while all eyes will be on US Federal Reserve Chair Jerome Powell when he discusses the outlook for the US economy later this week.

If central banks double down on the fact they will be keeping rates at or near zero at the short-end for years (the market is starting to doubt this), or that they will do more to keep long-term rates low, then gold may well bounce, providing either a temporary pause, or complete end to the recent corrective cycle.

DISCLAIMER

Past performance does not guarantee future results. The information in this article and the links provided are for general information only and should not be taken as constituting professional advice from The Perth Mint. The Perth Mint is not a financial adviser. You should consider seeking independent financial advice to check how the information in this article relates to your unique circumstances. All data, including prices, quotes, valuations and statistics included have been obtained from sources The Perth Mint deems to be reliable, but we do not guarantee their accuracy or completeness. The Perth Mint is not liable for any loss caused, whether due to negligence or otherwise, arising from the use of, or reliance on, the information provided directly or indirectly, by use of this article.