Gold rallies as geopolitical risks soar

Executive Summary

- Gold prices rallied 6% in February, ending the month back above USD 1,900 per troy ounce.

- Silver performed well too, rallying by 8%, while platinum and palladium prices also increased.

- Equity markets continued to correct, with the S&P 500 down 3% during February and falling by 8% during the year to date.

- Commodities continued to power higher, led by oil (+10% for the month, +28% year to date), with the Bloomberg Commodity index rallying another 6% during February.

- The Russian invasion of the Ukraine and the build up towards it was the main driver of markets. The war is likely to remain a key focus given its implications for inflation and growth expectations, as well as the path of monetary policy going forward.

Conflict, inflation and volatility drive gold higher

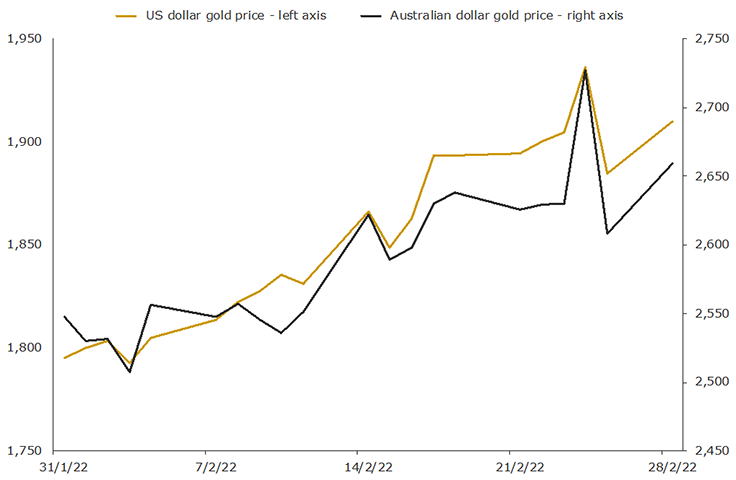

Gold prices rose in an almost uninterrupted fashion for most of February, as seen in the chart below. Multiple factors contributed to the rally, including higher than expected inflation readings in the United States, with CPI now +7.5% on a yearly basis. A continued pullback in equity markets was also supportive.

The main driver though was the build up towards and subsequent invasion of the Ukraine by Russia, which some, including UK Prime Minister Boris Johnson, see as having the potential to lead to “the biggest war in Europe since 1945”.

Daily US and Australian dollar gold prices per troy ounce February 2022

Source: World Gold Council

While gold was strong for most of the month, it did see a temporary pullback in prices late last week, driven in part by the belief that Russia would only face limited sanctions in response to its actions.

However, this proved short-lived, with news that Russian banks would be cut off from the SWIFT payments system, and that the Russian central bank would have some of its assets frozen.

Even Switzerland, famed for its political neutrality dating back more than two centuries to the 1815 Congress of Vienna, has moved to sanction Russia.

While we can only hope that hostilities do not escalate, the implications of the Russia-Ukraine conflict on the global economy and on financial markets are likely to be profound and long-lasting.

In the immediate term it’s noteworthy that;

- Inflation expectations are rising, with 5-year breakeven inflation rates increasing from 2.82% to 3.11% across the month.

- Growth is likely to take a hit, with the latest estimate from the Atlanta Fed’s GDPNow suggesting real GDP growth will be 0.00% for the first quarter of the year, down from their 0.6% projection just a few days ago.

- Questions will continue to be asked about just how aggressively central banks will be able to hike interest rates given the conflict in Ukraine, with a Bloomberg article noting “swaps linked to the Fed’s March 16 meeting dwindled to just 22 basis points of tightening on Tuesday. That suggests traders don’t even expect a full quarter-point hike -- a contrast from last month, when a half-point move was all but fully priced.”

Energy policy in Europe is also likely to change significantly, which is unsurprising given the reliance that the European Union has on Russia, with the latter providing the former almost 40% of its natural gas and 25% of its crude oil.

Precious metals the only place to hide?

All these factors raise the risk (though not the certainty) that the global economy is heading into a protracted period of stagflation, where growth rates falls well short of inflation.

Should that eventuate, history would suggest gold will be not only a clear market outperformer, but one of the few assets that delivers positive real returns.

This is evidenced in the table below, sourced from a 2021 Schroders research report on the impact that stagflation has on asset class returns.

Average real (inflation-adjusted) year on year total returns in stagflationary environments since 1973 (%)

US equities

US treasuries

US T-bills

Commodities

Gold

REITS

-1.5

0.6

0.4

15.0

22.1

6.5

Source: Schroders

Historical data like this reinforces why investors looking for protection and growth may wish to increase gold allocations going forward, with equities, cash and bonds (which make up the majority of the investments held in diversified portfolios today) having poor track records during periods of stagflation.

Gold’s role may be even more important this time around, given equities are far more expensively valued today compared to the last period of stagflation (the CAPE ratio for the S&P 500 was just 18.71 at the start of 1973, versus 37.47 at the start of 2022).

Debt levels are also more problematic this time around. While the US national debt to GDP ratio was just 33% back in 1973, it had risen to more than 120% by the end of last year.

This almost certainly limits the capacity of central banks to increase interest rates going forward, which would limit the ability of cash and bonds to protect wealth.

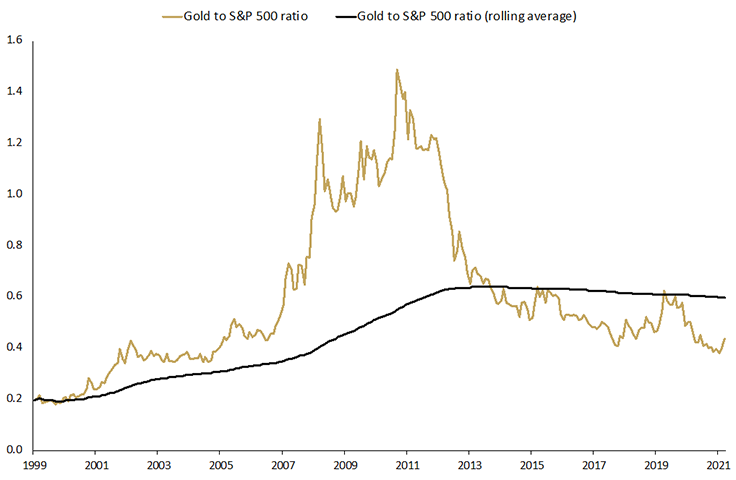

Gold outperforming equities by 13%

One indicator we are watching closely is the gold to S&P 500 ratio, which measures the number of shares in the S&P 500 (assuming the index represented one company) an investor can purchase for every ounce of gold they own.

Back in 2011, this ratio peaked at around 1.4, meaning an ounce of gold could buy 1.4 shares in the S&P 500. In the 10 years since then, the ratio fell significantly, largely driven by the 280% rally in the S&P 500 over this time, with gold up just 19%.

Movements in this ratio can be seen in the chart below, which covers the entire period since the turn of the century.

Gold versus the S&P 500

Source: The Perth Mint, World Gold Council, St Louis Federal Reserve

In the first two months of this year, the ratio has begun to climb, (from 0.38 to 0.44) with gold outperforming the S&P 500 by 13%.

While it’s too early to say that gold is entering an era where it will strongly outperform equities, it would not surprise should it do so.

At the very least, ratios like this suggest the long period of equity market outperformance is at, or near an end, and that investors may benefit from holding an allocation to gold going forward.

Currency bonus for Australian investors

For local investors, gold’s defensive qualities, which are again front of mind given current events, are typically enhanced by currency market impacts.

For local investors, gold’s defensive qualities, which are again front of mind given current events, are typically enhanced by currency market impacts.

This is because the Australian dollar typically declines in periods equity markets are weak. This decline boosts the return of gold priced in Australian dollars versus the return of gold priced in US dollars.

This is a subject The Perth Mint researched in detail as part of our latest investment whitepaper, which was published earlier this week.

Our findings suggest that since the turn of the century, this currency impact has been worth almost 1.2% in terms of enhanced portfolio returns Australian investors would get from holding gold in months Australian equities have declined.

Gold price moves when Australian equities fall - 2000 to 2020

Returns in months Australian equities fall

Average monthly returns (%)

US dollar gold price

0.82

Australian dollar gold price

2.01

Source: The Perth Mint, World Gold Council, RBA, Marketwatch

Outlook

Gold is likely to be driven in the short-term by the situation in the Ukraine, with higher volatility likely to be seen across a range of markets for now.

The demand picture is, however, very encouraging with bar and coin purchasing in Western markets at historically high levels.

Gold ETF investors are also now adding to their positions (after reducing them by approximately 5% in 2021), though so far, the inflows are relatively modest with holdings increasing just 2% for the year.

The bigger movements have been in the futures market, with gross long positioning by speculators +30% during February (+48% YTD), while net long positioning was +37% for the month (+94% YTD).

While this change in speculative positioning raises the risk that gold could see short-term pullbacks, the medium to long-term picture remains favourable, with the case for including gold in a portfolio significantly strengthened by the crisis in Ukraine and the impact it will have in the years ahead.

DISCLAIMER

Past performance does not guarantee future results. The information in this article and the links provided are for general information only and should not be taken as constituting professional advice from The Perth Mint. The Perth Mint is not a financial adviser. You should consider seeking independent financial advice to check how the information in this article relates to your unique circumstances. All data, including prices, quotes, valuations and statistics included have been obtained from sources The Perth Mint deems to be reliable, but we do not guarantee their accuracy or completeness. The Perth Mint is not liable for any loss caused, whether due to negligence or otherwise, arising from the use of, or reliance on, the information provided directly or indirectly, by use of this article.