Gold, Bitcoin and the Elon effect

“Bull markets are born on pessimism, grown on scepticism, mature on optimism, and die on euphoria” – John Templeton

It’s been just over three years since we last wrote about bitcoin, back when it was going through its first investment mania, with the price nearing USD 20,000 per coin at its peak.

From late 2017 through to March of last year, the bitcoin price collapsed, falling as low as USD 3,185 over this period, with investor interest and media coverage also waning.

No matter whether you think bitcoin is a Ponzi scheme, the future of money, or something in between, there is no doubting it is front page news again.

The decision by Elon Musk, CEO of US electric vehicle company Tesla, helped push the price above USD 50,000 per coin in February 2021.

Since early March 2020, when it was trading below USD 5,000, bitcoin has rallied by more than 900%, with ever more optimistic price forecasts being issued by the day.

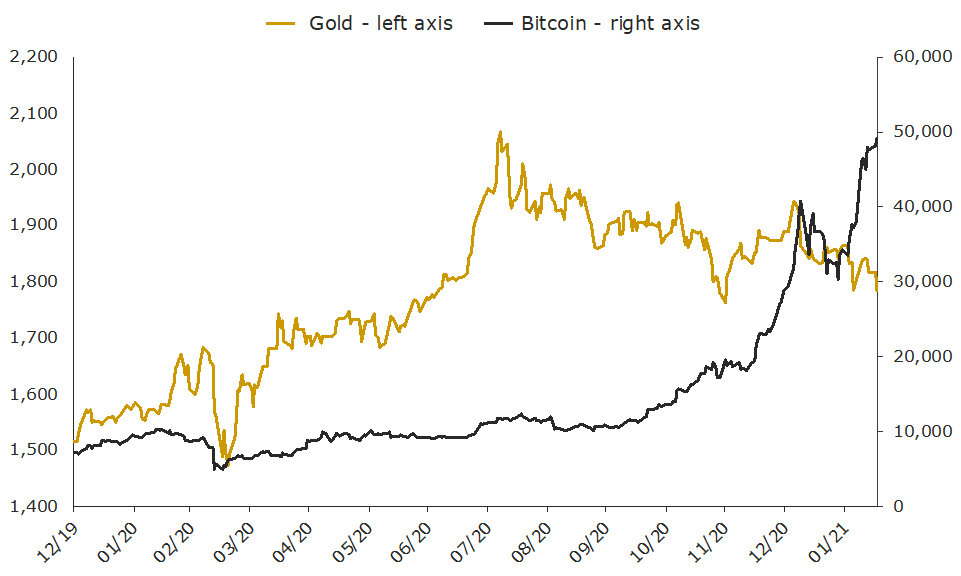

Given much of the rally in bitcoin has occurred since August, which has coincided with a long overdue pullback in gold (see chart below), there are no shortage of commentators stating that the precious metal is being usurped by its digital counterpart. Some have gone so far as to encourage investors to drop gold and reallocate to bitcoin instead.

Gold and Bitcoin prices – December 2019 to February 2021

Source: World Gold Council, LBMA, Coinmetrics, data to morning of 17 February 2021

In our latest report, Gold, Bitcoin and the Elon effect, we question this narrative and highlight the multiple attributes by which investors can, and indeed should, compare these two investments.

With one notable exception, gold would appear to have a handful of advantages that the world’s most famous cryptocurrency will never catch.

Here are some key insights to consider:

- Bitcoin beats gold hands down from the perspective of generating speculative returns in rapid fashion, but is 12 times more volatile than the precious metal.

- The gold market is significantly larger in terms of overall value, with a market capitalization that is more than 10 times the bitcoin market.

- The gold market is substantially more liquid, averaging approximately 90 times the daily turnover of the bitcoin market in 2020.

- Free storage options for gold are much lower risk than free bitcoin storage options, given the counterparty risk inherent in the latter.

- Gold is a lower cost investment than bitcoin, with gold ETPs like Perth Mint Gold (ASX:PMGOLD) offering gold exposure for 0.15% p.a., versus 1-2% p.a. for existing bitcoin products.

- Multiple uses of gold – for investment, as a reserve asset, as a display of wealth in jewellery form, and in industry, are far more diverse than bitcoin’s, which is almost exclusively used for speculation, with payment volumes across the cryptocurrency network declining in the last three years.

- Gold has a multi-millennia track record as a store of value and has been the best performing asset in equity market corrections over the past 50 years. In contrast, it is far too early to say that Bitcoin is a store of wealth. This is no fault of bitcoin per se, rather an acknowledgment that it has only existed in an era of low inflation, economic expansion (up until COVID-19), and a record bull market run in equities.

- Gold’s network effect is far stronger than bitcoin’s, best evidenced by the perpetual marketing of bitcoin itself as digital gold. Gold is not marketed as analog bitcoin.

- Bitcoin remains under threat, both from hard forks of the bitcoin network itself, as well as thousands of other cryptocurrencies, whereas gold’s status remains rock solid (pun intended).

- The gold market is far more decentralized than the bitcoin market, with the precious metal mined, refined, and owned by central banks, households and investors the world over. Bitcoin on the other hand is predominately held by a small group of owners, while mining is overwhelmingly concentrated in one country.

There are two extra points worth making, which have nothing to do with gold vs. bitcoin per se, but rather the idea that many corporations will follow Tesla’s lead and also invest part of their treasury into bitcoin.

The first point is that we remain unconvinced this will happen, as most CEOs and company boards will not willingly take on the risk it would bring into their business, while the attention it will by definition take away from core operations another factor to consider. It’s also not immediately clear why a business with excess cash wouldn’t just return it to shareholders, either via dividends or buybacks.

Secondly, if it does happen, we can’t help but feel it would represent a massive vote of no confidence in monetary policy settings. Rather than encouraging more capital investment, negative real rates would appear to be encouraging non-financial corporations to turn themselves into quasi-asset managers.

Note that none of the above should be seen as a bearish case for bitcoin per se. Whilst the parabolic price move is a bubble warning sign, and it’s hard to think of a more euphoric moment than the world’s richest man using company money to invest in this nascent asset class, we have no real view on where bitcoin is heading.

Rather, it’s an attempt at a balanced look at what the rise of cryptocurrency is telling us about financial markets and the economy, and the many attributes by which investors might judge both bitcoin and gold, which remain two vastly different investment propositions.

For a variety of reasons the precious metal will still likely be the preferred investment option for risk conscious investors looking to protect capital in the years ahead.

DISCLAIMER

Past performance does not guarantee future results. The information in this article and the links provided are for general information only and should not be taken as constituting professional advice from The Perth Mint. The Perth Mint is not a financial adviser. You should consider seeking independent financial advice to check how the information in this article relates to your unique circumstances. All data, including prices, quotes, valuations and statistics included have been obtained from sources The Perth Mint deems to be reliable, but we do not guarantee their accuracy or completeness. The Perth Mint is not liable for any loss caused, whether due to negligence or otherwise, arising from the use of, or reliance on, the information provided directly or indirectly, by use of this article.