What do you need to know about adding gold to your SMSF?

Interest in including gold as part of the superannuation investment is growing, but there are some key questions to ask to understand which options might be right for you.

Compulsory superannuation turns 30 this year, a milestone that means most working Australians should be building a solid nest egg for their retirement.

But those past 30 years haven’t been all clear sailing. The All Ordinaries has been negative in eight calendar years in the past three decades[1], while the younger S&P ASX200 has had four negative years [2] in the past 10.

In contrast, the AUD price of gold has had two negative calendar years in the past decade, helping to explain why there’s renewed focus on bullion as part of a superannuation portfolio.

Why gold?

For millennia, gold has been highly sought-after – initially because of its inherent value as a currency, in jewellery and as a safe investment during times of strife.

Increasingly it is also viewed as a safe option for superannuation funds and managed funds at times when other asset classes have faltered.

The past two years have seen surging interest in gold among exchange-traded fund investors [3] , even before the pandemic caused markets to become jittery.

As a hedge against market uncertainty and risk it is a long-term performer, and in a period of low real interest rates and negative yielding debt, gold’s safe haven reputation has been reinforced.

Investors who wish to explore gold as an option for superannuation can consider posing these questions to a financial adviser before making a commitment.

Is gold the right option for my investment?

An investment in physical gold does not pay a dividend like a blue-chip ASX stock so potential investors should be aware that growth comes from an appreciation in the price of spot gold — and therefore the value of their gold investment.

But historically it has been an excellent hedge against inflation because the gold price tends to rise when the cost-of-living increases [4].

Investors also flock to gold when faced with uncertainty and confusion – the turbulence in US politics, global trade wars and the COVID-19 pandemic are just three reasons why today’s gold price is so strong.

No two super funds are the same but shares and property are largely the financial vehicles of choice for most growth-focused retirement investments, be they self-managed or through an institution, because they offer diversity, liquidity (in the case of shares) and annual income in the way of dividends or rental payments.

Depending on risk appetite, funds will also have varying levels of investment in cash, fixed income, infrastructure, unlisted equities and ‘other’.

Physical gold – that is, actual gold compared with investments in gold mining companies – falls into the ‘other’ category, which makes it an attractive option for further safely diversifying a self-managed superannuation fund.

The data is not definitive, but it is believed that less than 0.1% of all Australian superannuation assets [5] are currently invested in physical gold. This may be because it is not widely seen as a growth asset that compounds in the way that blue-chip shares can.

Manager, Listed Products and Investment Research at The Perth Mint, Jordan Eliseo, says the role of gold and other precious metals in a portfolio depends on risk appetite and their preferred investment balance.

“Some investors look to put five to 10 per cent, and sometimes up to 20 per cent of their portfolio into gold and precious metals,” he says.

“But it depends on a range of factors, including what else they own in their portfolio.”

How long should I hold my investment?

Independent advice should be sought from a licensed financial adviser before making any investment. However, generally speaking, gold is considered a long-term asset.

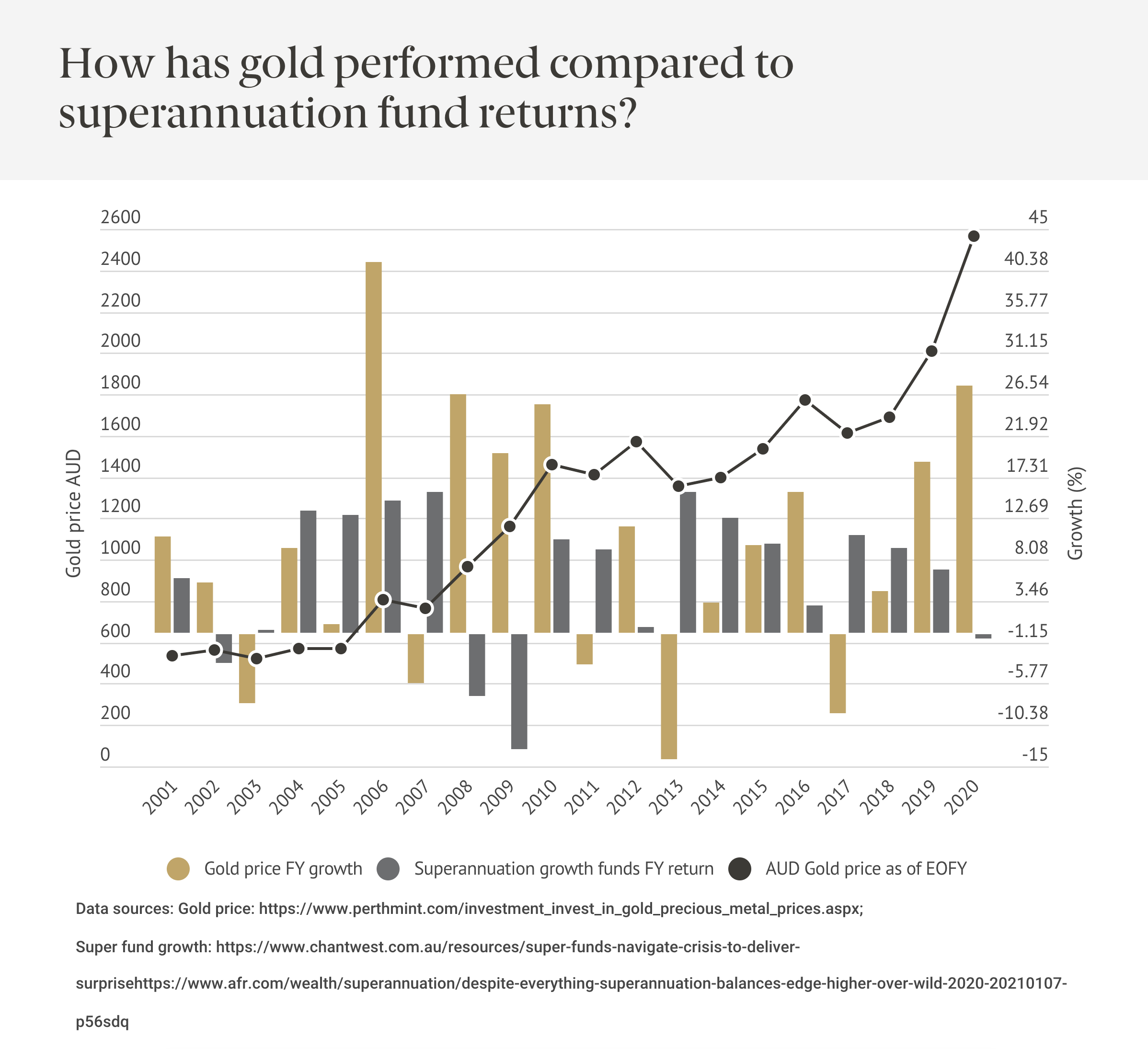

Looking at gold’s historical performance, in years where the growth of managed funds has stalled or declined, the value of the precious metal has been strong. It’s a pattern of growth that many have come to accept as a given – gold’s value grows when shares falter.

Even better, in years where super funds have grown, the value of gold hasn’t necessarily declined. In fact, of the 10 years between 2000 and 2019 during which super funds grew by 9 per cent or more, gold outperformed them in five.

“Gold is positively correlated to stock markets when they rise, so the price tends to rise alongside the stock market, but it's negatively correlated to the stock market when the stock market falls,” he says.

“Now, it doesn’t go up by as much as stocks when stocks are going up, so you make money, but you just don't make as much money as if you were completely in shares.

“The price also tends to rise when the stock market's going down.

“Now, it doesn't go up as much in a strong market, but the beauty of gold is that when the market declines, gold has historically still performed.”

How would I buy physical gold?

There are different ways of buying physical gold for a SMSF, but a depository solution is considered best practice, because of the reporting and audit obligations for SMSFs.[6]

So before a purchase is made, consideration needs to be given to storage and appropriate insurance.

The Perth Mint’s Depository service allows investors to easily buy bullion – of different sizes and values, to suit the individual investor – and have it safely stored in the mint's high-security vaults in Australia, all covered by a guarantee from the Government of Western Australia.

Allocated storage allows you to purchase The Perth Mint’s physical bullion products, which the mint segregates in its high-security vaulting facilities under your name[7]. The Perth Mint charges a fee for keeping allocated gold secure in its vault. The gold remains readily available for inspection, pick-up or delivery — unlike unallocated gold, which is essentially a purchase into the mint’s pool of working metal.

Unallocated storage is the most popular option among The Perth Mint’s depository clients because there are no ongoing storage fees[8]. But there are also no specific bars or coins recorded against individual clients because the metal backing their account is pooled. It is not possible for a client to view these types of gold holdings.

Should investors wish to purchase and store gold in an external location such as in their home or in a bank safe, The Perth Mint suggests the investor takes out adequate insurance, mainly against theft. Insurance must be in the name of the SMSF and not a personal policy, such as a home and contents policy [9].

What if I don’t want physical gold?

An alternative to physical bullion is investing in a right to gold, through our ASX-listed product PMGOLD. The product is backed by physical bullion, and each unit represents 1/100th of an ounce at gold.

As the gold price moves, so does PMGOLD, and if you decide you would rather change to physical bullion, it can be redeemed for any of The Perth Mint’s bullion bars.

Another significant advantage for SMSF trustees is PMGOLD which can be bought and sold through a stockbroker or share trading account with the same ease and convenience as investing in shares.

Are there any tax implications for investment?

Australia does not have any import or export restrictions on precious metals, including gold, so clients are free to move their investment in and out of the country [10].

The purchase of gold, as well as silver and platinum, is exempt from Australia’s 10 per cent GST if it meets certain conditions, including:

- A purity of 99.5 per cent or higher

- Capable of being traded on the international bullion market

- Bearing a mark of a recognised manufacturer identifying and guaranteeing the fineness and quality of the gold

The Perth Mint's bullion coins and bars meet the above definition, which is why purchasing privately minted bars and coins carries a greater investment risk.

Where do I start?

The Perth Mint provides a comprehensive guide to getting started with gold in your SMSF, which also strongly recommends that you seek personal financial advice before investing in gold [11].

If it is the right fit for your super investment, The Perth Mint has a range of investment options including online and offline depository accounts, which many investors use to access gold for their own SMSFs.

The Perth Mint’s Depository program gives clients direct access to experienced bullion dealers who can quote a competitive live spot price to buy or sell precious metal.

If you believe physical gold will not sit comfortably within your SMSF but you want to make sure you have exposure to a millennia-strong history of strong investment returns, ask The Perth Mint about our other, non-physical gold investment products.

SOURCES

[1] https://stooq.com/q/d/?s=%5eaor

[2] https://www2.asx.com.au/about/market-statistics/historical-market-statistics

[3] https://www.perthmint.com/

[4] https://www.investopedia.com/articles/basics/08/reasons-to-own-gold.asp

[5] http://www.perthmintbullion.com/au/blog/blog/19-12-16/Gold_and_superannuation.aspx

[6] http://www.perthmintbullion.com/au/blog/blog/19-04-10/Why_how_now_SMSF_trustees_are_turning_to_gold.aspx

[9] https://www.walshaccountants.com/superannuation-your-pot-of-gold/

[10] https://www.youtube.com/watch?v=CzVDLAmoUkQ

[11]https://www.perthmint.com/invest/information-for-investors/information-for-smsf-investors/

DISCLAIMER

Past performance does not guarantee future results. The information in this article and the links provided are for general information only and should not be taken as constituting professional advice from The Perth Mint. The Perth Mint is not a financial adviser. You should consider seeking independent financial advice to check how the information in this article relates to your unique circumstances. All data, including prices, quotes, valuations and statistics included have been obtained from sources The Perth Mint deems to be reliable, but we do not guarantee their accuracy or completeness. The Perth Mint is not liable for any loss caused, whether due to negligence or otherwise, arising from the use of, or reliance on, the information provided directly or indirectly, by use of this article.