Wall Street bets on silver squeeze as gold eases

Precious metal markets were mixed in January, with gold down marginally, while silver rose. While long-term drivers remain supportive, the current euphoria in financial markets, an increase in bond yields, and rising optimism regarding a huge economic stimulus package from Washington, have acted as short-term headwinds for precious metals, which remain in a consolidation phase.

Summary of market movers:

- The USD gold price fell marginally in January, ending the month at USD 1,863.80 per troy ounce (/oz)

- Silver ended the month above USD 27/oz, rising by more than 3%, with the gold to silver (GSR) ratio finishing January at 68

- Risk assets continued to rally, with equities and cryptocurrencies hitting all-time highs

- A mania in meme-stocks and rumours of a short squeeze in silver captured market attention in late January, with volatility surging in select company share prices

- The announcement of an additional AUD 100 billion in Quantitative Easing (QE) from the Reserve Bank of Australia (RBA), and a decline in iron prices may mark a top in the Australian dollar, which traded as high as USD 0.78 in January.

Full report - January 2021

The price of gold eased marginally in January, falling by 1.26% to end the month at USD 1863.80/oz. Silver fared better, rising by 3.5% to USD 27.42/oz, with the GSR falling to 68 by the end of last month, after starting the year at 71.

Multiple factors contributed to the soft start to the year for gold, including the change in the White House, and Democratic Party wins in the Georgia Senate election runoff, which raised hopes of a circa USD 2 trillion economic stimulus package.

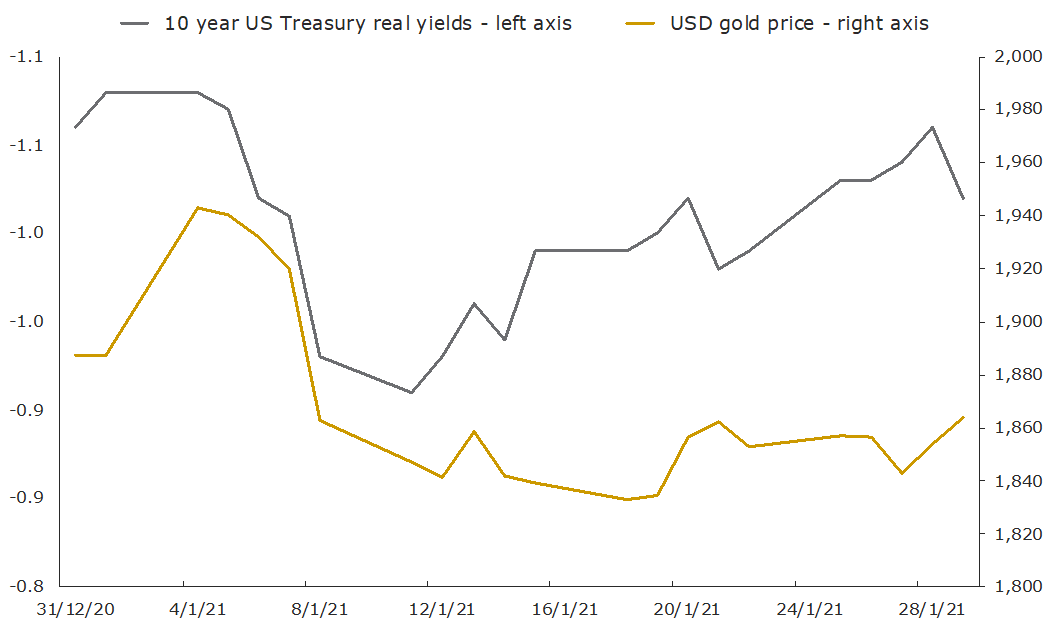

This was enough to see yields on US treasury securities rise by almost 25% (from +0.93% to +1.15% on the US 10 year) by mid-January. Real yields increased as well, though are still negative, with these moves in the bond market coinciding with an approximately 6%, or USD 110/oz fall in the USD gold price intra-month.

The chart below highlights this, showing movements in the USD gold price (gold line) and the real yield on a US 10-year treasury (black line), across the course of January. Note that yields are inverted on the chart, that is, a falling in the black line means real yields are rising, and vice-versa.

Source: The Perth Mint, World Gold Council, US Treasury

The other factor holding gold back in January was the continued euphoria building in financial markets, with the Citigroup Panic/Euphoria model hitting all-time highs in January 2021.

Furthermore, a range of metrics from stock market capitalization to GDP ratios, to price/earnings and price/sales ratios for the S&P 500 suggest the US stock market is now as or more expensive than it has ever been, with investment legend Jeremy Grantham warning investors last month that markets have now “matured into a fully-fledged epic bubble”.

Signs of excess, which are no doubt temporarily limiting the safe haven appeal of precious metals, weren’t limited to traditional asset classes. Cryptocurrencies also hit all-time highs, with Bitcoin trading above USD 40,000 per coin in early January, though it did pullback as the month unfolded.

Wall Street Bets, Gamestop and the silver squeeze

The most eye-catching development in financial markets in the first few weeks of 2021 was the rise of Wall Street Bets (WSB), a reddit sub-thread of retail investors that discuss investment opportunities in financial markets.

Over the course of January and early February, a number of people that were members of WSB encouraged the broader group to aggressively buy shares and call options on listed companies that hedge funds were shorting, meaning the hedge funds would benefit if the stock prices fell.

The idea was that by aggressively buying shares and options, the WSB could force a “short squeeze” and a “gamma squeeze” (note we have links at the bottom of this article for those who’d like to read more about these terms) combined.

This would see financial institutions that were either short the shares in those companies, or who had sold call options over those companies need to aggressively buy stock as well, to manage their risk.

And for a few short days, the strategy “worked” spectacularly.

The most high-profile company caught up in this was GameStop (ticker: GME), which over the course of January rose from below USD 20 per share to more than USD 450 per share (based on intraday pricing). A very select group of people purportedly made millions from the price spike in GME through the use of derivatives.

Sensing an opportunity to make vast gains in a short period of time, as well as get one up on hedge fund and institutional investors, the WSB group has supposedly grown to more than seven million members. In many ways this should not have been unexpected, given the tailwinds that have driven this phenomenon, including:

- Many people with excess time on their hands due to COVID-19 lockdowns and higher unemployment

- “Free” money from government stimulus checks

- “Free” trading on certain investment platforms

- Rising inequality and frustration with “elites”, particularly those in financial markets

Toward the end of last month, the attention of the WSB community turned to precious metals, with an attempt to create a silver squeeze generating lots of attention in financial markets and the news media.

Whilst there are a number of reasons to remain confident in the outlook for silver in the months and year ahead, the silver squeeze narrative is at best a distraction, and at worst a risk for investors, at least in the short-term.

Firstly, it needs to be stated that liquidity in the global silver market, and precious metal markets generally, is an order of magnitude more significant than liquidity in any of the individual stocks caught up in the recent WSB mania. That makes it a much harder market for anyone to “squeeze”, especially retail investors with smaller amounts of investment capital.

Secondly, whilst some investors have bought into a narrative of commercial banks being short silver, they are typically only looking at futures market data, which is public information updated on a regular basis, to draw that inference.Those investors, and certain sections of the precious metal community that relentlessly promote this narrative are completely ignoring the fact there is a large over-the-counter (OTC) market in precious metals. Given this fact, whilst certain financial institutions might be short silver (or gold) futures, they may well, and indeed are most likely long those precious metals in the OTC market at any given time.

Thirdly, it is worth pointing out that whilst there may be shortages of silver in specific form (i.e. small bars and coins) and in specific locations, that in no way evidences a shortage of silver itself.

Fourthly, it is worth pointing out that at present, managed money positions in the silver market are net long, with data as at 26 January showing a gross long position of 67,430 contracts and a gross short position of 23,110 contracts.

This means that on balance speculators are betting prices will rise rather than fall. That rather destroys the WSB narrative of hurting hedge funds by buying silver, given the hedge fund community would benefit from a rising silver price.

As a final comment on this phenomenon, while undoubtedly some of the WSB community will have purchased silver (either in bar, coin, ETF or derivative form) in the last week or so, we also think there is a good chance most of the increased buying has actually been driven by existing silver investors.

It also looks like the price spike in companies like GME is well and truly over, with the share price closing just above USD 92 on Wednesday 3 February, down more than 80% from the highs seen during this phenomenon.

Outlook

Moving forward, there are some risks to the outlook for precious metals. ETF inflows have slowed (for gold) considerably, as has central bank buying, though both are still positive, whilst consumer demand in key markets like China, India and other parts of Asia and the Middle East will take some time to recover fully.

The potential for the USD to rally after a more than 13% decline over most of 2020 could also be a short-term headwind for precious metals, with the dollar index up 2% since early January.

Finally, silver’s correction in the past 48 hours despite the silver squeeze and WSB narrative also suggests the precious metal market may consolidate for a while longer, even if the longer-term strategic case for investing in these metals remains undiminished.

The x-factor for gold, and indeed for financial markets as a whole, is COVID-19. While everyone hopes that we have seen the worst and that 2021 marks the beginning of a ‘post COVID’ world, there are no guarantees.

Mutations are beginning to develop, while meaningful parts of the global economy remain locked down. Even the best-case scenario, which would see a successful rollout of vaccines around the world, represents an enormous logistical and political challenge, with global economic output unlikely to catch up to its pre COVID-19 trajectory for years.

Markets are pricing in a best-case scenario right now. If the situation deteriorates, expect risk assets to suffer, policy makers to deploy even more stimulus, and safe haven assets like gold to catch a bid.

Combined, these potential tailwinds indicate that precious metal prices are likely to remain biased to the upside for some time to come. Most importantly, from a portfolio management perspective, assets like gold in particular continue to offer unique diversification benefits to investors, which should see investment flows supported going forward.

FURTHER INFORMATION

Short Squeeze

https://www.investopedia.com/terms/s/shortsqueeze.asp

Gamma Squeeze

https://www.swfinstitute.org/news/83341/what-is-a-gamma-squeeze-in-the-context-of-stock-trading

Silver gross short position

https://ycharts.com/indicators/comex_silver_combined_managed_money_short_positions

Silver gross long position

https://ycharts.com/indicators/comex_silver_combined_managed_money_long_positions

DISCLAIMER

Past performance does not guarantee future results. The information on this page and the links provided are for general information only and should not be taken as constituting professional advice from The Perth Mint. The Perth Mint is not a financial adviser. You should consider seeking independent financial advice to check how the information on this page relates to your unique circumstances. The Perth Mint is not liable for any loss caused, whether due to negligence or otherwise, arising from the use of, or reliance on, the information provided directly or indirectly, by use of this page.